Digital Underwriting in Banking and Insurance: AI Risk Assessment

Underwriting has always been a critical function in both banking and insurance. It determines whether an applicant qualifies for a loan, policy, or financial product and evaluates the level of risk associated with each application. Traditionally, underwriting has relied on manual document review, fragmented data sources, and human expertise to assess risk. While this approach ensures regulatory compliance and careful evaluation, it also introduces operational challenges such as slow processing times, inconsistent decision-making, and high operational costs.

In today’s digital economy, these limitations are increasingly evident. Customers expect faster service and near-instant decisions, while financial institutions must process growing volumes of applications under stricter compliance requirements. As a result, many organizations are turning to digital underwriting to modernize their risk assessment processes.

By combining automation, artificial intelligence, and advanced analytics, digital underwriting enables institutions to streamline underwriting workflows while maintaining strong governance. Instead of relying entirely on manual reviews, organizations can process data more efficiently and make consistent risk decisions supported by intelligent systems.

Understanding Digital Underwriting in Financial Services

A Data-Driven Model for Risk Assessment

Digital underwriting refers to the use of digital technologies to automate and enhance the evaluation of financial and insurance risk. Rather than relying solely on manual assessments, digital underwriting systems integrate artificial intelligence, automated data processing, and predictive analytics to analyze applicant information and generate risk insights.

In practice, digital underwriting connects several stages of the application lifecycle into one continuous workflow. Customer data can be captured through online portals, mobile applications, or conversational interfaces, while supporting documents are processed using intelligent recognition technologies.

Supporting Human Expertise with Intelligent Systems

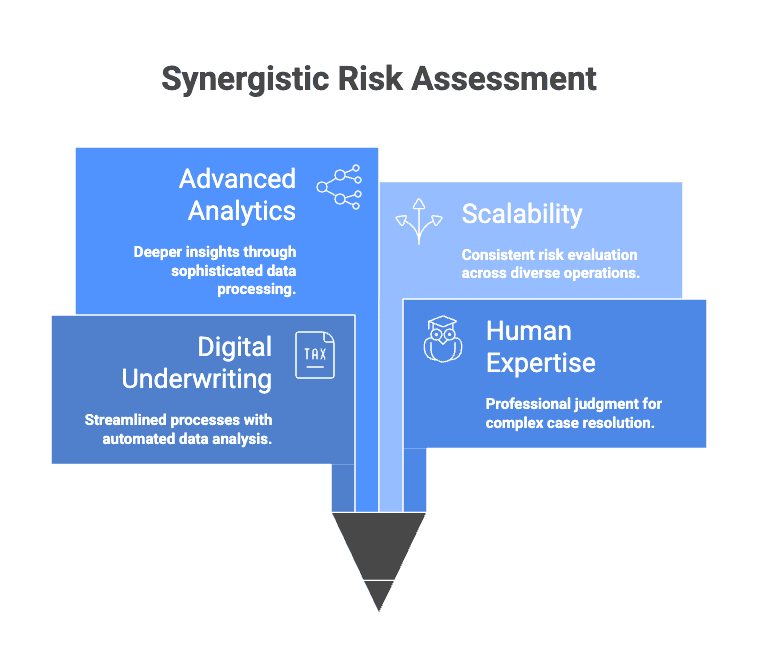

Digital underwriting does not replace the expertise of professional underwriters. Instead, it supports their work by providing deeper analytical insights and reducing administrative workload. Automated data extraction and risk analysis allow underwriters to focus on complex cases that require professional judgment.

By combining human expertise with advanced analytics, digital underwriting enables financial institutions to build more scalable and consistent risk evaluation frameworks.

Core Technologies Enabling Digital Underwriting

Intelligent Data Collection and Customer Interaction

The first stage of digital underwriting involves collecting reliable applicant information. Many financial institutions now use conversational interfaces such as chatbots and voicebots to guide customers through digital application processes. These systems help capture structured information while validating entries in real time.

By digitizing the intake process, digital underwriting platforms improve both data quality and user experience. Customers can complete applications more easily, while institutions receive standardized information that supports accurate risk analysis.

Document Intelligence and Automated Data Extraction

Document processing has traditionally been one of the most time-consuming stages in underwriting. Applications often include identity documents, financial statements, forms, and other supporting materials. Manual verification of these documents can delay decision-making and introduce potential errors.

Digital underwriting addresses this challenge through intelligent document processing technologies. OCR systems enhanced with machine learning automatically extract key information from documents and convert it into structured data that underwriting engines can analyze. This automation reduces operational delays and improves the reliability of the underwriting process.

AI-Driven Risk Scoring and Decision Engines

At the center of digital underwriting platforms are AI-powered risk scoring engines. These systems analyze applicant profiles using predictive models, historical data, and predefined underwriting rules. Instead of relying solely on static criteria, digital underwriting systems evaluate patterns across large datasets to identify potential risk indicators.

Machine learning models can uncover relationships between variables that may not be visible during manual analysis. By incorporating these insights, digital underwriting platforms provide more accurate and consistent risk assessments while maintaining transparency for regulatory compliance.

A Modern Digital Underwriting Workflow

Digital Application Intake

A modern digital underwriting workflow begins with digital application intake. Applicants submit their information through online platforms or mobile channels where automated systems validate entries and ensure that required fields are completed. This process establishes a structured dataset that forms the basis for further evaluation.

Document Processing and Risk Analysis

After the intake stage, submitted documents are processed by intelligent document recognition systems. These systems extract relevant information and verify document authenticity, allowing digital underwriting platforms to eliminate manual data entry.

Once the information is validated, underwriting engines perform risk analysis using artificial intelligence models and predefined policies. The system evaluates financial data, historical patterns, and behavioral indicators to generate a risk score representing the applicant’s profile.

Automated Decisioning and Policy Issuance

Following risk evaluation, digital underwriting platforms perform automated decisioning. Applications that meet predefined criteria may be approved instantly, while higher-risk cases can be referred to experienced underwriters for additional review.

Once a decision is made, approved applications proceed to automated issuance. Contracts, insurance policies, or loan agreements can be generated digitally and delivered directly to customers, completing the underwriting cycle in a significantly shorter timeframe.

Strategic Benefits of Digital Underwriting

Operational Efficiency and Faster Decision-Making

One of the most significant advantages of digital underwriting is the ability to accelerate processing times. Automated document analysis, data extraction, and risk scoring enable financial institutions to evaluate applications in minutes rather than days.

This efficiency allows organizations to scale their underwriting operations while maintaining consistent risk standards.

Improved Risk Accuracy and Customer Experience

Digital underwriting also improves the accuracy of risk evaluation. AI-driven models can analyze large datasets and identify patterns that manual reviews might overlook. This leads to more reliable underwriting decisions and reduced exposure to operational risk.

From a customer perspective, digital underwriting improves the onboarding experience. Faster approvals, fewer documentation errors, and clearer processes contribute to greater customer satisfaction and trust.

Implementing Digital Underwriting in Regulated Environments

System Integration and Data Governance

Successful implementation of digital underwriting requires seamless integration with existing financial systems. Platforms must connect with core banking infrastructure, policy administration systems, and customer relationship management tools to ensure efficient data flow.

Strong data governance is also essential. Because underwriting decisions involve sensitive financial and personal data, institutions must implement strict security frameworks and comply with regulatory standards governing data protection.

Deployment Strategies for Compliance and Control

Many financial institutions choose to deploy digital underwriting systems within their own infrastructure rather than relying on external SaaS platforms. On-premise deployment allows organizations to maintain full control over sensitive data while ensuring compliance with regulatory requirements.

This approach supports stronger security management and enables institutions to adapt underwriting systems to their internal governance frameworks.

The Future of Digital Underwriting

Predictive Risk Intelligence

The future of digital underwriting will be shaped by advances in artificial intelligence and data ecosystems. As analytical models become more sophisticated, underwriting systems will evolve from reactive evaluation toward predictive risk intelligence.

Future digital underwriting platforms are likely to incorporate alternative data sources such as open banking information, behavioral analytics, and connected device data. These insights will allow institutions to detect emerging risk patterns earlier and develop more accurate risk profiles.

Personalized Financial Products

Digital underwriting will also support the development of more personalized financial products. By analyzing detailed customer data, financial institutions can design insurance policies and lending solutions tailored to individual needs and risk characteristics.

This shift toward personalization will strengthen customer relationships while improving portfolio performance and long-term risk management.

Conclusion: Digital Underwriting as a Strategic Capability

Digital underwriting is rapidly becoming a foundational capability for financial institutions seeking to modernize risk management and operational efficiency. By combining artificial intelligence, intelligent document processing, and automated decision engines, digital underwriting allows organizations to process applications faster while maintaining transparent and consistent risk evaluation.

As financial institutions continue to adopt advanced analytics and new data sources, digital underwriting will evolve into a predictive risk intelligence framework that supports better decision-making and more personalized financial services.

References

- McKinsey & Company. (2024). Insurance 2030: The impact of AI and advanced analytics on underwriting transformation. McKinsey & Company.

- Deloitte. (2023). AI-powered underwriting: Transforming risk assessment in insurance and financial services. Deloitte Insights.

- Accenture. (2024). AI-driven underwriting: Reimagining insurance risk assessment through automation and analytics. Accenture Financial Services Research.

Get in Touch

Stay Connected with sourceCode To receive regular updates on industry insights and expert perspectives, make sure to Follow sourceCode on LinkedIn now! For collaboration opportunities, cutting-edge tech solutions, or to explore career possibilities with us, please visit our website: sourcecode.com.au