Governing the Machine: Why 2026 Is the Board's Year for Responsible AI in APAC Banking

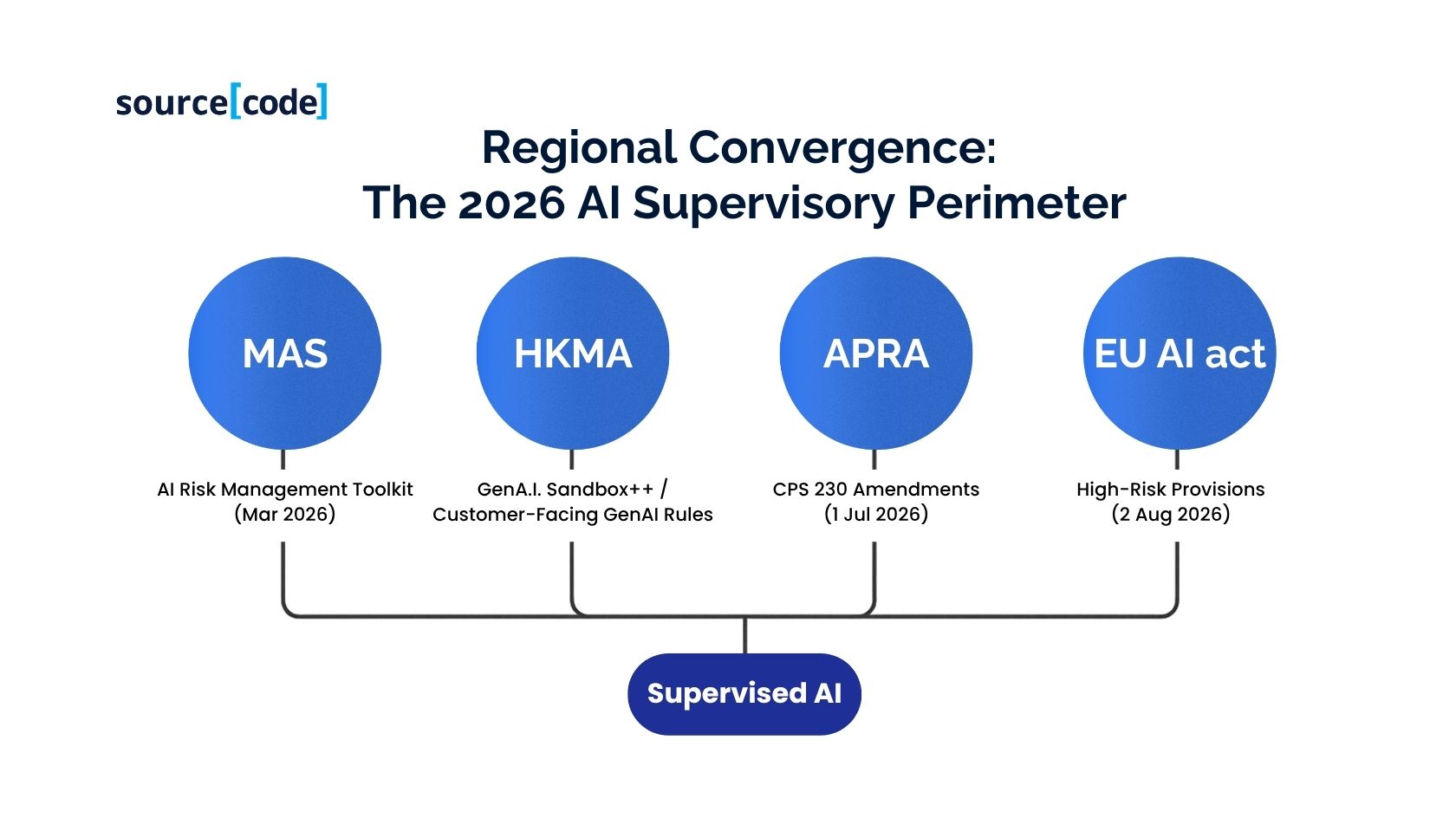

Between March and July 2026, three of Asia-Pacific's most influential prudential regulators - the Monetary Authority of Singapore (MAS), the Hong Kong Monetary Authority (HKMA) and the Australian Prudential Regulation Authority (APRA), moved decisively from principles-based guidance to supervisory-ready expectations for artificial intelligence. MAS released an AI Risk Management Toolkit and Operational Handbook; HKMA extended its GenA.I. Sandbox++ and hardened customer-facing requirements; APRA finalized targeted amendments to CPS 230 and issued an unusually blunt industry letter warning that AI risk practices are not keeping pace with adoption.

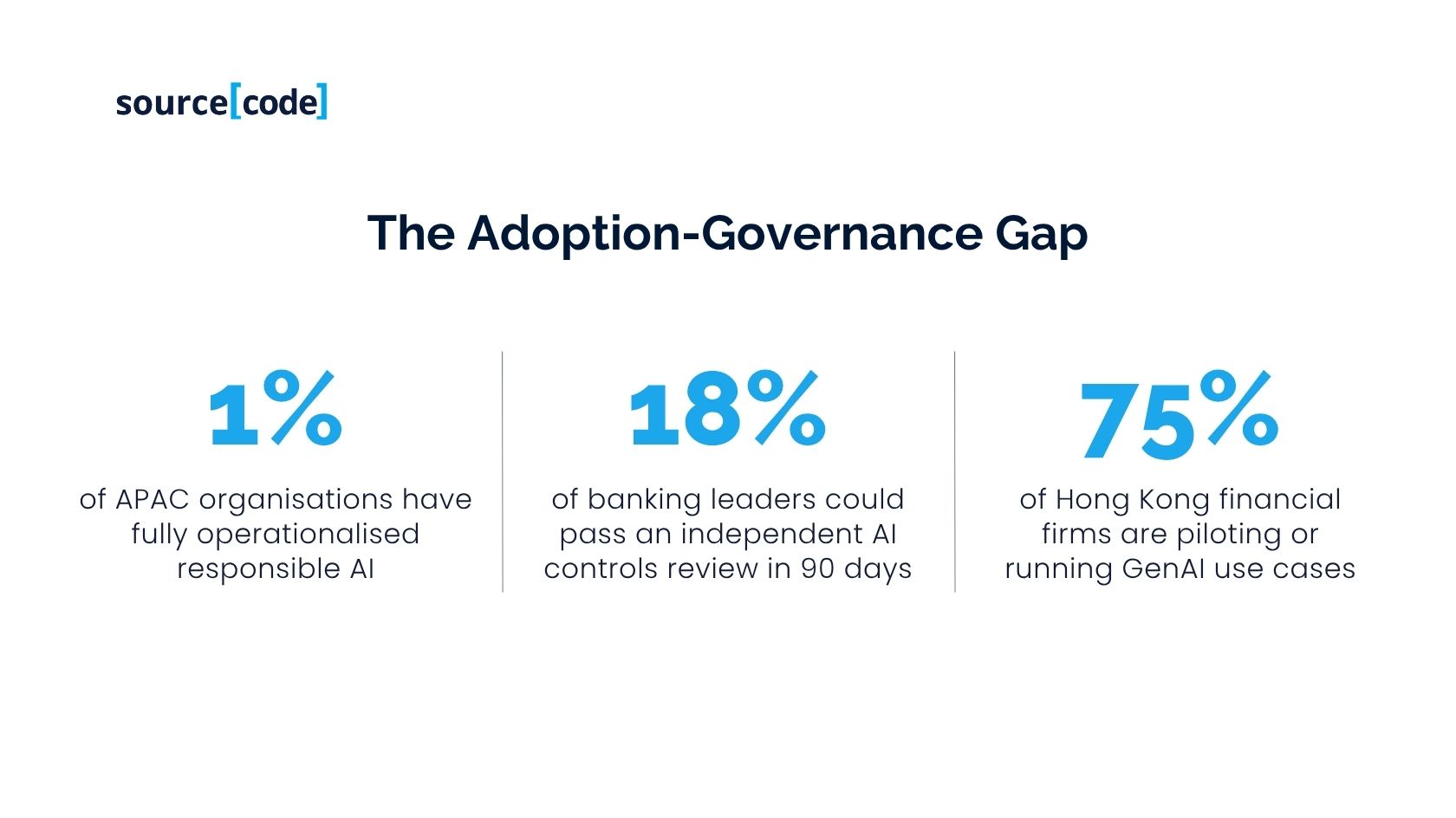

The signal is consistent and unambiguous. AI is now an enterprise-risk class subject to board accountability, and 2026 is the year when supervisors will begin testing controls, not merely reviewing intent. Yet the data suggests that most APAC financial institutions are not ready. Only 1% of organizations in the region report fully operationalized responsible AI (Intelligent CIO APAC, 2026), while 18% of banking leaders globally say they could pass an independent review of their AI controls within 90 days (BCG, 2026). This article maps the regulatory perimeter, quantifies the readiness gap, and offers a pragmatic operating model for boards, chief risk officers and chief data officers who must close it before the next supervisory cycle.

Introduction

For much of the past three years, AI in banking was a chief-technology-officer conversation. It has now become a chief-risk-officer conversation, and as of mid-2026, a board-committee conversation. The shift is regulatory as much as commercial. In November 2018 MAS published the FEAT Principles (Fairness, Ethics, Accountability, Transparency) as a voluntary framework; by 2026, those same principles anchor formal supervisory expectations under the MAS Guidelines on AI Risk Management, complete with an Operational Handbook that details expected controls across the AI life cycle (MAS, 2026). Hong Kong and Australia have moved on parallel timelines.

For BFSI executives across APAC and Southeast Asia, the question is no longer whether to institutionalize responsible AI, but how to do so at the speed at which the business is deploying generative and agentic systems. That gap between adoption velocity and governance maturity is the strategic risk of the next twelve months.

A Regional Regulatory Convergence

Three regional developments define the 2026 operating environment.

Singapore: from principles to supervision. In March 2026, MAS published the AI Risk Management Toolkit, centered on an Operational Handbook that "details a range of actions designed to implement the principles in the Guidelines" and increases the likelihood that MAS will assess AI governance as part of routine inspections and thematic reviews (Hogan Lovells, 2026). The Guidelines apply to all MAS-regulated financial institutions: local and foreign banks, insurers, capital markets services firms, payment service providers and licensed fintechs (Protiviti Singapore, 2026). Singapore is widely regarded as the de facto standard-setter for AI supervision in the region.

Hong Kong: customer-facing GenAI under a human-in-the-loop mandate. HKMA guidance now requires banks deploying customer-facing generative AI to retain a "human-in-the-loop" for decision-making, offer customers an opt-out from GenAI-mediated interactions, disclose the purposes and limitations of GenAI, and document the demographic impact of algorithms used in credit scoring (Gibson Dunn, 2026). In March 2026, HKMA, SFC, IA and MPFA jointly launched an expanded GenA.I. Sandbox++ spanning banking, capital markets, wealth, insurance and MPF (HKMA, 2026). A recent Hong Kong Institute for Monetary and Financial Research (HKIMR) survey found that 75% of firms have implemented or are actively piloting at least one GenAI use case, signaling a market where governance must scale alongside experimentation.

Australia: operational resilience meets AI-specific risk. CPS 230 (Operational Risk Management) came into force on 1 July 2025, and on 30 April 2026 APRA finalized targeted amendments taking effect on 1 July 2026 (Norton Rose Fulbright, 2026). More significantly, APRA warned that "governance, risk management, assurance and operational resilience practices are not keeping pace with the scale, speed and complexity of AI adoption," singling out prompt injection, data leakage, insecure integrations and the manipulation of autonomous AI agents as pressing threats (Shadow AI Watch, 2026). CPS 234 (Information Security), CPS 220 (Risk Management) and CPS 230 are the existing standards through which APRA expects AI to be governed, an important nuance for institutions that have been waiting for a stand-alone AI prudential standard.

Layered over these regional regimes is the extraterritorial reach of the EU AI Act, whose high-risk system provisions take effect on 2 August 2026. The Act applies to any provider or deployer whose AI system outputs are used inside the EU, meaning APAC banks with EU customers, correspondent relationships or capital-markets touchpoints must complete conformity assessments in parallel (Deloitte Luxembourg, 2024).

The Adoption-Governance Gap

The data tells a consistent story: adoption is running ahead of governance.

-

Adoption. APAC's banking sector is described as the region's most advanced AI adopter, with 83% of APAC CFOs citing AI as a key force reshaping finance and 72% expecting significant impact within three years (Wolters Kluwer, 2026).

-

Maturity. McKinsey's 2026 State of AI Trust reports that average responsible-AI maturity has risen to 2.3 out of 5 up from 2.0 in 2025, but only about a third of organizations report maturity of three or higher in strategy, governance or agentic-AI oversight (McKinsey, 2026a).

-

Operationalization. Only 1% of APAC organizations have fully operationalized responsible AI, with most relying on partial, ad hoc or newly defined measures (Intelligent CIO APAC, 2026).

-

Control confidence. Just 18% of banking leaders are fully confident they could pass an independent review of their AI controls within 90 days (Global Association of Risk Professionals, 2026).

-

Root cause. 66% of AI vendors, 46% of regulators and 40% of industry respondents cite data availability and quality as the leading barrier to safe deployment (Cambridge Centre for Alternative Finance, 2026).

Beneath these numbers sits a structural problem. Model-risk-management (MRM) frameworks in most APAC banks were designed for statistical, deterministic models with bounded use cases. Generative and agentic systems are neither. They exhibit behavioral drifts, produce non-deterministic outputs, integrate deeply with third-party oundation models, and increasingly act on the world with limited human intervention. Compliance organisations built for stable models are now supervising systems whose bbehaviorchanges with each fine-tune or prompt update.

Key Trends Shaping the 2026-2027 Horizon

Four trends deserve board attention.

1. AI is being reclassified as an enterprise-risk category. BCG's 2026 outlook recommends elevating tech, data and cyber resilience into enterprise governance through board-level oversight, and critically locating AI oversight within the board risk committee rather than the technology committee (BCG, 2026). This is a governance-topology change with real consequences: charters, delegated authorities, escalation paths and reporting cadences all need to be redrawn.

2. Third-party AI is the next concentration risk. APRA has explicitly flagged that "AI capabilities are increasingly embedded within software and platforms, limiting an entity's ability to independently assess model performance, bias, resilience and security" (Shadow AI Watch, 2026). Vendor risk management frameworks that were built for cloud infrastructure and SaaS are now inadequate for foundation-model dependencies.

3. Agentic systems demand new monitoring infrastructure. McKinsey has argued that agentic AI requires monitoring that "can detect behavioral drift in production, escalate anomalies in real time, and maintain audit trails", capabilities that most banks' MRM stacks do not currently possess (McKinsey, 2026b).

4. The talent model is being rewritten by regulators. HKMA, together with the Hong Kong Association of Banks and the Hong Kong Institute of Bankers, has published the "Capacity Building for Future Banking, 2026-2030" guidelines, formalizing expectations for AI-literate risk, audit and compliance functions (HKMA, 2026).

A Control Blueprint for APAC BFSI

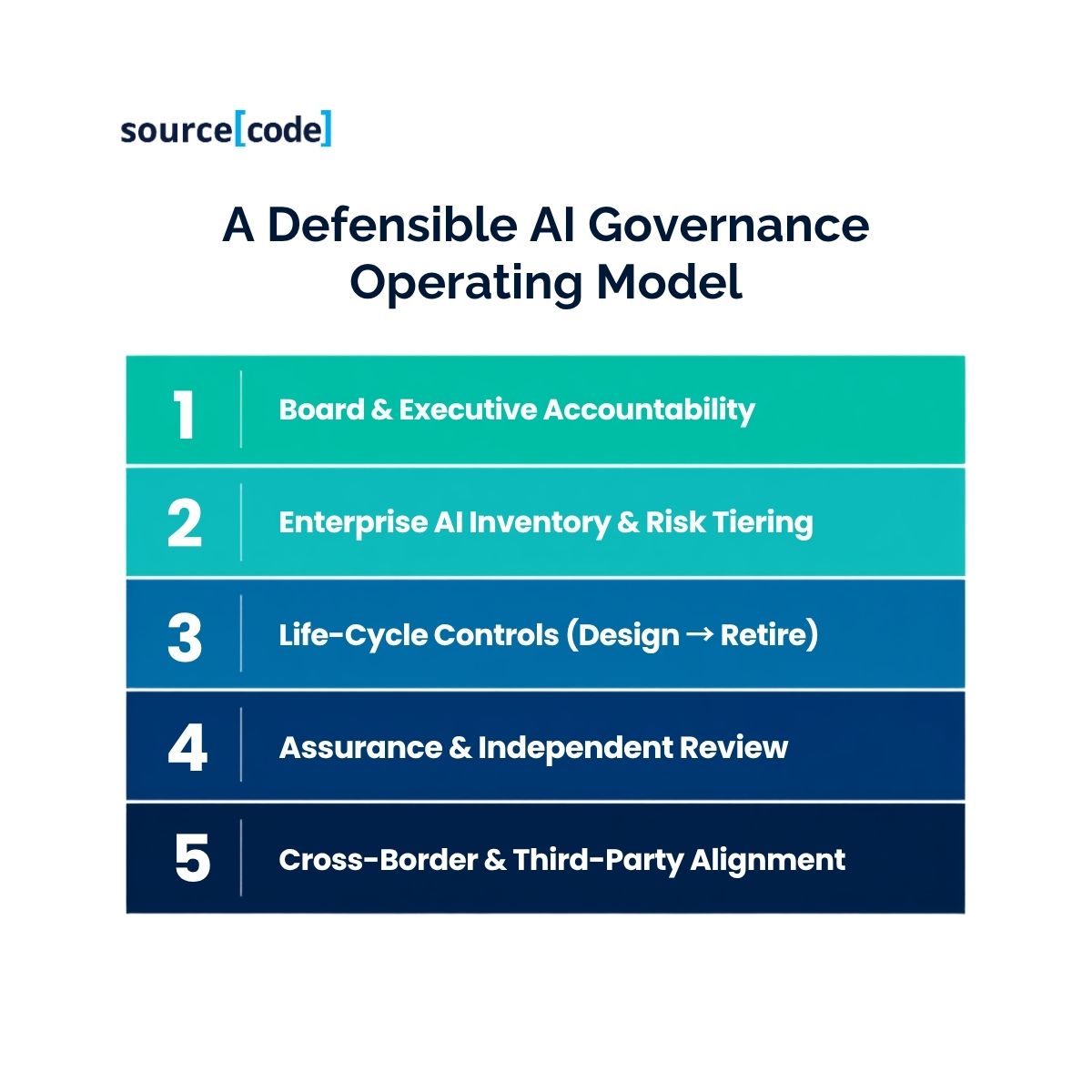

A defensible AI governance operating model in 2026 rests on five interlocking layers. Each maps to specific supervisory expectations already published by MAS, HKMA or APRA.

Layer 1 - Board and executive accountability. A named board committee (typically Risk) owns AI risk appetite; a designated executive (frequently the CRO or a Chief AI Officer reporting to the CRO) owns operational accountability. Quarterly reporting includes inventory-by-risk-tier, drift and incident metrics, third-party concentration exposure and control effectiveness.

Layer 1 - Board and executive accountability. A named board committee (typically Risk) owns AI risk appetite; a designated executive (frequently the CRO or a Chief AI Officer reporting to the CRO) owns operational accountability. Quarterly reporting includes inventory-by-risk-tier, drift and incident metrics, third-party concentration exposure and control effectiveness.

Layer 2 - Enterprise AI inventory and risk tiering. No institution can govern what it cannot see. A single system of record, covering models, agents, prompts, retrieval pipelines, vendor components and shadow AI, is now table stakes. Risk tiering should be aligned to both regional guidelines and the EU AI Act's high-risk classification to reduce duplicated compliance effort.

Layer 3 - Life-cycle controls (design, build, validate, deploy, monitor, retire). MAS's Operational Handbook, HKMA's customer-facing GenAI expectations and APRA's CPS 230 operational-risk requirements converge on the same life-cycle spine. The differentiating capability is evidence generation at design time - bias tests, red-team results, prompt-injection defences, human-in-the-loop protocols, captured in a form auditors and supervisors can review without re-running the model.

Layer 4 - Assurance and independent review. Given that only 18% of banks say they could pass an independent review today (BCG, 2026), building second-line and third-line AI assurance capability is now urgent. This includes standardised testing protocols for fairness, robustness, security and explainability, and an assurance calendar aligned to the supervisor's inspection cycle.

Layer 5 - Cross-border and third-party alignment. Institutions operating across Singapore, Hong Kong, Australia and (increasingly) the EU must reconcile overlapping obligations. A single, layered control taxonomy with jurisdiction-specific overlays reduces cost and audit fatigue.

Real-world Signals from the Region

-

MAS's Veritas Initiative and Project MindForge have progressively translated FEAT principles into implementable methodologies, culminating in the 2026 Toolkit, the clearest signal yet that Singapore intends to supervise, not merely encourage (MAS, 2026).

-

HKMA's 75%-piloting statistic (HKIMR) is now paired with mandatory customer opt-out and demographic-impact documentation, meaning execution risk is concentrated at the customer interface (Gibson Dunn, 2026).

-

Australia's APRA industry letter cites specific attack vectors: prompt injection, data leakage and the manipulation of autonomous agents that few Australian banks currently test for as part of standard security assurance (Shadow AI Watch, 2026).

-

Across ASEAN, regulators including Bank Negara Malaysia, Bank of Thailand and the Bangko Sentral ng Pilipinas are actively studying MAS's approach as a template, accelerating a regional convergence that reduces the argument for jurisdiction-specific control architectures.

Actionable Recommendations for BFSI Leaders

For the Board and CEO

-

Charter AI oversight to the Risk Committee, with a standing agenda item and quarterly metrics pack.

-

Approve an AI risk appetite statement covering permitted use cases, prohibited use cases, third-party foundation-model dependencies and human-in-the-loop thresholds.

-

Commission an independent AI controls review within the next two supervisory cycles.

For the Chief Risk Officer -

Extend Model Risk Management to cover generative and agentic systems, with explicit behavioral-drift and prompt-injection controls.

-

Reconcile CPS 230 / MAS Guidelines / HKMA circulars into a single control taxonomy to reduce redundant testing.

-

Build a supervisor-ready evidence pack per high-risk use case.

For the Chief Data and AI Officer -

Establish a single enterprise AI inventory covering shadow AI and vendor components.

-

Embed evaluation, red-teaming, and fairness testing into CI/CD pipelines.

-

Rationalize foundation-model concentration risk through a multi-model reference architecture.

**For the Chief Information Security Officer ** -

Extend security assurance to cover prompt injection, data exfiltration via context windows, and agent-tool misuse.

-

Update third-party risk assessment templates to include foundation-model provenance, training-data disclosures, and model-card reviews.

The sourceCode Perspective

Governance is only defensible when it is engineered into the operating fabric of the bank, not appended to it. Across our BFSI engagements in APAC, we consistently observe that the institutions closing the adoption-governance gap fastest are those treating responsible AI as a platform-engineering problem rather than a policy problem. They invest in enterprise AI inventories, evaluation harnesses, evidence-capture pipelines, and drift-monitoring infrastructure with the same rigor applied to core banking or payments platforms.

sourceCode partners with banks, insurers and fintechs across the region to design and build the technical spine of AI governance: model registries and inventories, evaluation and red-team frameworks, retrieval and prompt-security layers, monitoring for behavioral drift, and third-party model assurance workflows. Our engineering teams work alongside second-line risk and compliance functions to translate MAS, HKMA and APRA expectations into production-grade controls that a supervisor can inspect on any given day.

The organizations that will lead APAC BFSI over the next decade are not those with the largest AI budgets, but those whose governance is credible enough to let them deploy at speed with confidence.

Conclusion

The regulatory posture across MAS, HKMA and APRA has converged on a shared conclusion: AI is a first-order enterprise risk, and boards will be held accountable for its supervision. The 2026 window is decisive because the supervisory infrastructure: toolkits, sandboxes, prudential standards and industry letters, is now sufficiently mature for inspection. Institutions that build a defensible AI operating model this year will be positioned to accelerate deployment through 2027 and beyond. Those that do not will find their commercial ambitions constrained by supervisory findings, remediation programmes and reputational cost.

The task is neither hopeless nor optional. It is a design problem, and design problems reward institutions that treat governance as engineering.

Looking to translate MAS, HKMA and APRA expectations into a production-grade AI control environment? Talk with sourceCode about designing an AI governance operating model that lets your bank move faster, not slower.

FAQ

What is the MAS AI Risk Management Toolkit? Published in March 2026, the Toolkit, anchored by an Operational Handbook, translates the MAS Guidelines on AI Risk Management into concrete supervisory-ready control expectations across the AI life cycle.

Does APRA have a stand-alone AI prudential standard? No. APRA has confirmed that AI risk is governed through existing standards - principally CPS 230 (Operational Risk Management), CPS 234 (Information Security) and CPS 220 (Risk Management), as amended and enforced in 2025-2026.

Are APAC banks in scope for the EU AI Act? Yes, if their AI-system outputs are used within the EU. High-risk provisions take effect on 2 August 2026 and apply extraterritorially to non-EU providers and deployers.

Which board committee should own AI risk? Leading practice and BCG's 2026 recommendation, is to locate AI oversight within the Board Risk Committee rather than the Technology Committee, reflecting AI's classification as an enterprise-risk category.

What is the fastest way to close the AI governance gap? Establish an enterprise AI inventory, tier by risk, wire life-cycle controls into engineering pipelines, and commission an independent controls review aligned to the local supervisor's inspection cycle.

References

Boston Consulting Group, 2026. Risk and Compliance 2026: Refining Oversight for a Volatile, AI-Driven World. Boston: BCG. Available at: https://www.bcg.com/publications/2026/refining-oversight-for-a-volatile-ai-driven-world [Accessed 10 July 2026].

Cambridge Centre for Alternative Finance, 2026. 2026 Global AI in Financial Services Report - Adoption, Impact and Risks. Cambridge: Cambridge Judge Business School. Available at: https://www.jbs.cam.ac.uk/faculty-research/centres/alternative-finance/publications/2026-global-ai-in-financial-services-report/ [Accessed 10 July 2026].

Deloitte Luxembourg, 2024. EU AI Act adopted by the Parliament: What's the impact for financial institutions? Available at: https://www.deloitte.com/lu/en/Industries/investment-management/perspectives/european-artificial-intelligence-act-adopted-parliament.html [Accessed 10 July 2026].

Gibson Dunn, 2026. Hong Kong Monetary Authority Issues Guidance on Gen-AI Use in Customer-Facing Applications and Use of Artificial Intelligence in Tackling ML/TF. Available at: https://www.gibsondunn.com/hong-kong-monetary-authority-guidance-on-gen-ai-use-in-customer-facing-applications-and-use-of-ai-in-ml-tf/ [Accessed 10 July 2026].

Global Association of Risk Professionals (GARP), 2026. From Black Boxes to Boardrooms: How Banks Must Govern Artificial Intelligence. Available at: https://www.garp.org/risk-intelligence/culture-governance/black-boxes-boardrooms-260220 [Accessed 10 July 2026].

Hogan Lovells, 2026. From Principles to Practice: Maturing AI Supervision in Singapore's Financial Sector. Available at: https://www.hoganlovells.com/en/publications/from-principles-to-practice-maturing-ai-supervision-in-singapores-financial-sector [Accessed 10 July 2026].

Hong Kong Monetary Authority, 2026. Regulators launch GenA.I. Sandbox++ to foster A.I. innovation across financial services. Press release, 5 March. Available at: https://www.hkma.gov.hk/eng/news-and-media/press-releases/2026/03/20260305-3/ [Accessed 10 July 2026].

Intelligent CIO APAC, 2026. Addressing the AI governance gap in Asia Pacific. Available at: https://www.intelligentcio.com/apac/2026/05/20/addressing-the-ai-governance-gap-in-asia-pacific/ [Accessed 10 July 2026].

McKinsey & Company, 2026a. State of AI Trust in 2026: Shifting to the Agentic Era. Available at: https://www.mckinsey.com/capabilities/tech-and-ai/our-insights/tech-forward/state-of-ai-trust-in-2026-shifting-to-the-agentic-era [Accessed 10 July 2026].

McKinsey & Company, 2026b. How financial institutions can improve their governance of gen AI. Available at: https://www.mckinsey.com/capabilities/risk-and-resilience/our-insights/how-financial-institutions-can-improve-their-governance-of-gen-ai [Accessed 10 July 2026].

Monetary Authority of Singapore, 2026. MAS Partners Industry to Develop AI Risk Management Toolkit for the Financial Sector. Media release. Available at: https://www.mas.gov.sg/news/media-releases/2026/mas-partners-industry-to-develop-ai-risk-management-toolkit-for-the-financial-sector [Accessed 10 July 2026].

Norton Rose Fulbright (Global Regulation Tomorrow), 2026. APRA finalises targeted amendments to CPS 230 Operational Risk Management. Available at: https://www.regulationtomorrow.com/2026/05/apra-finalises-targeted-amendments-to-cps-230-operational-risk-management/ [Accessed 10 July 2026].

Protiviti Singapore, 2026. MAS AI Governance for Financial Institutions. Available at: https://www.protiviti.com/sg-en/blogs/mas-ai-governance-guidelines-risk-management [Accessed 10 July 2026].

Shadow AI Watch, 2026. APRA Warns Banks AI Risk Controls Are Falling Behind. Available at: https://shadowaiwatch.com/governance/apra-ai-risk-industry-letter-step-change-2026/ [Accessed 10 July 2026].

Wolters Kluwer, 2026. Future Ready CFO Report - APAC Findings. Reported in Yahoo Finance. Available at: https://finance.yahoo.com/sectors/technology/articles/wolters-kluwer-future-ready-cfo-011500228.html [Accessed 10 July 2026].